There’s a myth going around that you need to hide, trick, or bypass the system to trade crypto in India. That’s not true. You don’t need to avoid restrictions-you need to follow them. India hasn’t banned cryptocurrency. It’s made rules, and if you follow them, you’re completely legal.

India Didn’t Ban Crypto-It Taxed It

Back in 2018, the Reserve Bank of India (RBI) tried to block banks from dealing with crypto exchanges. That didn’t last. In 2020, India’s Supreme Court threw out that ban. Since then, crypto isn’t illegal-it’s regulated. And the biggest rule? You pay taxes.

As of 2025, the Income Tax (No. 2) Bill replaced the old 1961 law. Now, every crypto trade-whether you bought Bitcoin, traded Ethereum for Solana, or sold an NFT-is taxable. The government doesn’t care if you use a local app or a global one. What matters is: did you report it? Did you pay?

The tax rate? 30% on all gains. No deductions. No offsetting losses. If you bought Bitcoin at $30,000 and sold it at $50,000, you owe 30% on the $20,000 profit. That’s $6,000. Plus, there’s a 1% Tax Deducted at Source (TDS). Every time you trade on a registered exchange, they take 1% off the transaction value automatically. No exceptions.

Compliance Isn’t Optional-It’s the Only Way

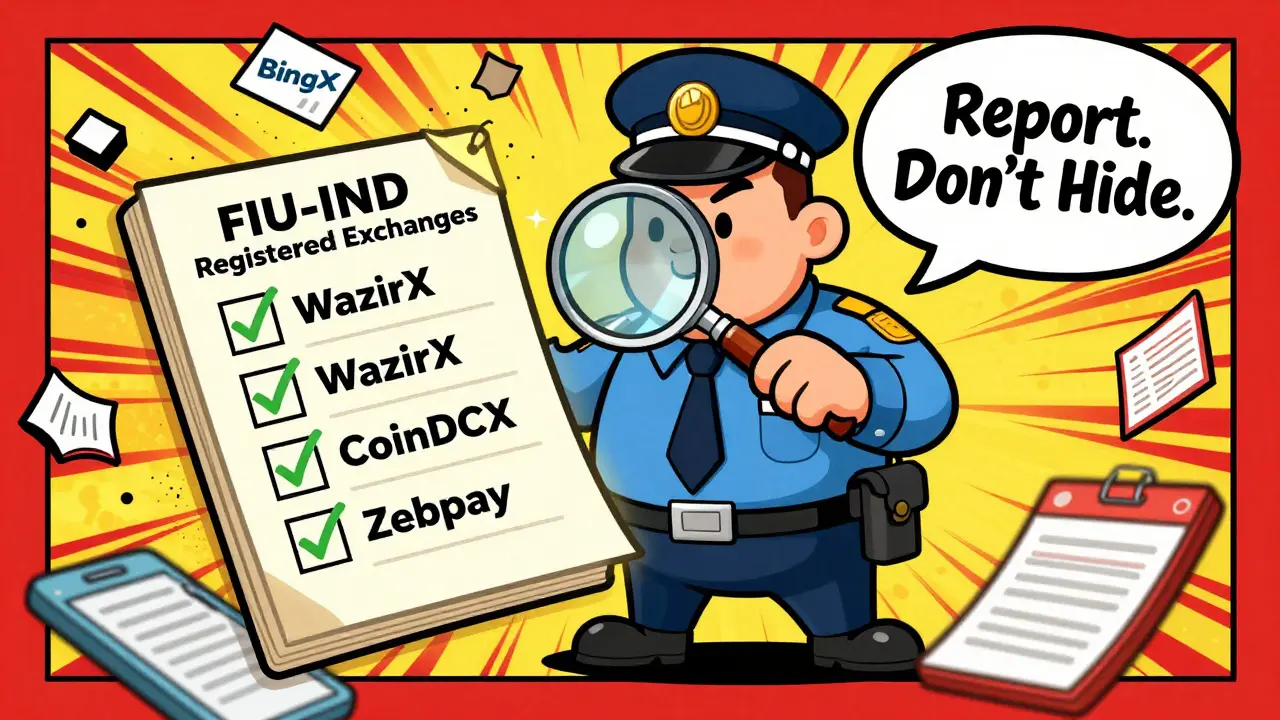

Trying to hide crypto income or use unregistered platforms? That’s where trouble starts. The Financial Intelligence Unit India (FIU-IND) is watching. They don’t care if you use Phantom Wallet or MetaMask. If money flows through a platform that hasn’t registered with them, you’re at risk.

As of 2025, over 50 crypto exchanges are officially registered with FIU-IND. That includes big names like Binance, Coinbase, WazirX, CoinDCX, and Zebpay. These platforms do three things:

- Verify your identity (KYC)

- Track every transaction

- Report suspicious activity

They also automatically deduct the 1% TDS and give you a tax statement at year-end. That’s your proof of compliance. If you use one of these platforms, you’re covered. If you use one that isn’t registered-like BingX or LBank, which were shut down for non-compliance-you’re not just risking fines. You’re risking a tax notice, a legal inquiry, or worse.

Keep Records Like Your Life Depends On It

India’s tax law says you must keep records of all crypto transactions for six years. That means every buy, sell, swap, and transfer. Not just the big ones. Even if you traded $10 of Dogecoin for Shiba Inu, it counts.

How do you do it? Simple:

- Use only FIU-IND registered exchanges.

- Download your transaction history every month.

- Save it in a spreadsheet with dates, amounts, prices in INR, and whether it was a buy, sell, or swap.

- Track wallet addresses if you send crypto off-exchange (like to a hardware wallet).

Why? Because if the tax department asks for proof, you need to show where the money came from and where it went. No records? You’ll be assumed guilty. And the penalty? Up to 300% of the unpaid tax.

Don’t Try to Outsmart the System

You’ll see posts online: "Use P2P to avoid TDS," or "Send crypto through a friend’s account." That’s not clever. That’s dangerous.

Peer-to-peer (P2P) trading is legal in India-but only if the platform is registered. If you use an unregistered P2P app, you’re not avoiding tax-you’re hiding it. And the government can trace blockchain transactions. They’ve done it before.

Same with crypto-to-crypto swaps. If you trade Bitcoin for Ethereum on an unregistered platform, the tax department still sees it as a taxable event. They don’t care if you didn’t convert to INR. Any transfer of value is a sale.

And don’t think using a VPN to access Binance Global will help. Binance India operates under local rules. If you’re in India, you’re under Indian law. The government doesn’t care if you’re using a foreign server. They care about your IP address, your bank account, and your tax filings.

What Happens If You Don’t Comply?

Two things: penalties and audits.

The Income Tax Department has been running targeted crypto audits since 2023. They cross-check data from registered exchanges with your income tax return. If you didn’t declare crypto gains, they’ll find it. They already have access to data from 50+ platforms. They’re not guessing-they’re matching numbers.

If you’re caught:

- You pay the 30% tax, plus interest.

- You pay a penalty of up to 100% of the tax due.

- You could be investigated for money laundering if large, unexplained transfers show up.

There are real cases. In 2024, a trader in Bangalore was fined ₹42 lakh ($50,000) for not declaring $180,000 in crypto gains over two years. He didn’t go to jail-but he lost half his savings.

What You Should Do Instead

Here’s the real path forward:

- Use only FIU-IND registered exchanges (WazirX, CoinDCX, Zebpay, Binance India).

- Enable KYC and keep your profile updated.

- Download your annual tax report from the exchange.

- Report all crypto income under "Income from Other Sources" in your ITR.

- Keep records for six years.

- Consult a tax advisor who understands crypto-don’t rely on YouTube tutorials.

That’s it. No hacks. No tricks. No hidden wallets. Just clean, documented, legal trading.

The Future Isn’t About Avoiding Rules-It’s About Following Them

India isn’t trying to kill crypto. It’s trying to control it. The government wants to stop money laundering, track tax evasion, and bring crypto into the financial system-not out of it.

At the G20 summit in 2023, India pushed for global crypto reporting standards. They’re aligning with the Crypto-Asset Reporting Framework (CARF), which means in the next few years, your crypto data will be shared automatically with tax authorities worldwide.

That’s not a threat. It’s a signal. The game has changed. The winners aren’t the ones who hide. They’re the ones who document, report, and pay.

The Indian crypto market is still growing. In 2024, it was worth $6.6 billion. People are still buying, trading, and investing. Why? Because the rules are clear now. You know what to do. You just have to do it.

Leslie Cox

February 23, 2026 AT 17:46Derek Sasser

February 24, 2026 AT 08:19Neeti Sharma

February 24, 2026 AT 18:15Nadia Shalaby

February 26, 2026 AT 02:33Fiona Monroe

February 28, 2026 AT 01:13Molley Spencer

February 28, 2026 AT 15:20John Fuller

February 28, 2026 AT 21:24Lucy Simmonds

March 2, 2026 AT 03:27Dana Sikand

March 3, 2026 AT 08:44Nicki Casey

March 5, 2026 AT 06:00Jessica Carvajal montiel

March 6, 2026 AT 03:24maya keta

March 6, 2026 AT 17:09Curtis Dunnett-Jones

March 7, 2026 AT 04:10Lilly Markou

March 7, 2026 AT 17:46McKenna Becker

March 8, 2026 AT 05:59precious Ncube

March 9, 2026 AT 02:18Jan Czuchaj

March 10, 2026 AT 12:11Tracy Peterson

March 11, 2026 AT 06:31George Suggs

March 11, 2026 AT 18:54KingDesigners &Co

March 13, 2026 AT 09:25Felicia Eriksson

March 13, 2026 AT 17:38aaron marp

March 15, 2026 AT 00:56Patrick Streeb

March 15, 2026 AT 05:28Tracy Whetsel

March 17, 2026 AT 02:51Michael Teague

March 18, 2026 AT 16:15