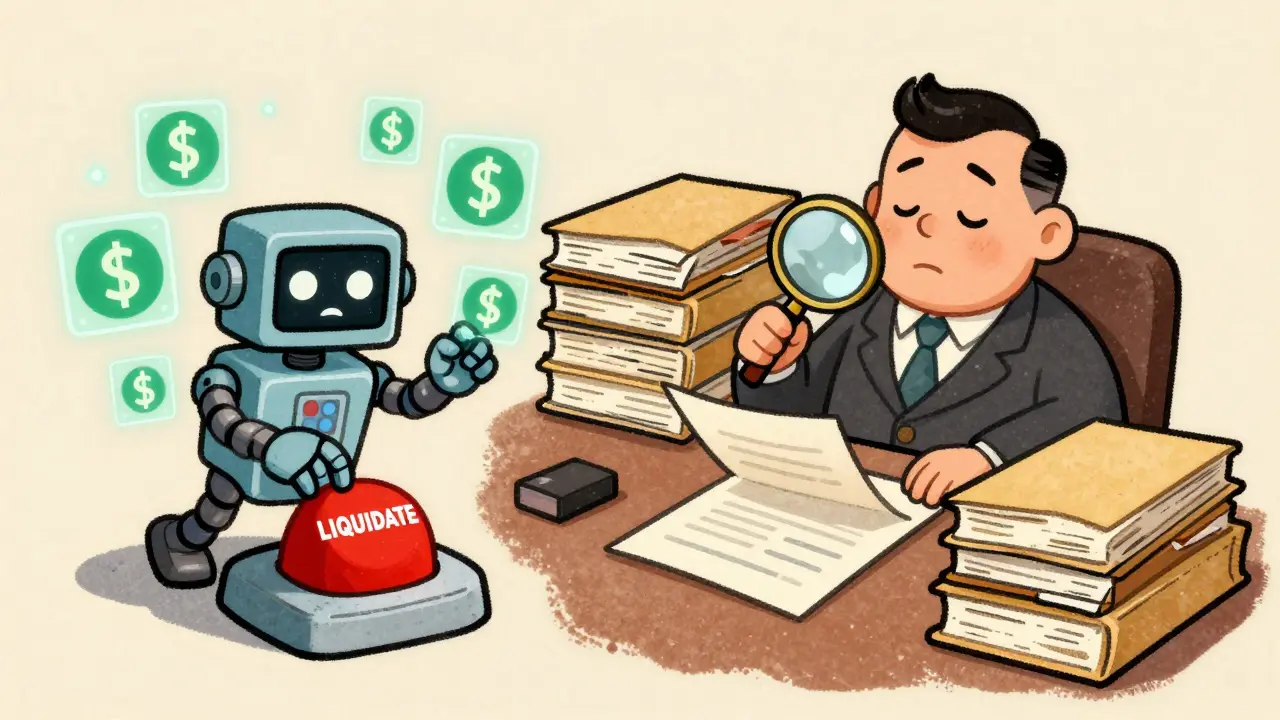

Imagine waking up to find that the assets you pledged to secure a loan have been sold off by a computer program without you even getting a phone call. In the world of digital finance, this isn't a nightmare-it's a Tuesday. Whether you are dealing with a high-tech smart contract or a government-backed business loan, the core goal of liquidation is the same: ensuring the lender doesn't lose money when a borrower can't pay back what they owe.

The way this happens varies wildly. In traditional banking, it's a slow, paperwork-heavy process involving lawyers and appraisals. In Decentralized Finance a blockchain-based form of finance that does away with traditional intermediaries like banks, it happens in milliseconds via code. Understanding the collateralized loan liquidation process is essential for anyone putting their assets at risk to gain liquidity.

The Basics: What is a Collateralized Loan?

At its simplest, a collateralized loan is a deal where you give the lender something of value (the collateral) to hold onto. If you pay back the loan with interest, you get your asset back. If you don't, the lender sells that asset to cover the debt. The magic number here is the Collateral Ratio, which is the value of your collateral compared to the amount you borrowed. If you borrow $100 and put up $150 in assets, your ratio is 150%.

Liquidation kicks in when that ratio drops too low. This usually happens for two reasons: either the value of your collateral crashes (like a sudden dip in crypto prices) or you fail to make your scheduled payments. Once you hit the "liquidation threshold," the lender has the legal or programmatic right to seize and sell your assets.

How Liquidation Works in DeFi

In DeFi, there is no loan officer to call you and ask for a payment plan. Everything is handled by Smart Contracts-self-executing code on a blockchain. Most DeFi protocols set a strict threshold, often around 110%. If your collateral ratio dips below this, you become eligible for liquidation.

Here is the actual step-by-step of a DeFi liquidation:

- Monitoring: The protocol constantly checks the current market price of your collateral using an "oracle" (a data feed).

- Trigger: The moment the price drops and your ratio hits the threshold, the smart contract marks your position as "liquidatable."

- The Liquidator: External actors, called liquidators, watch for these opportunities. They pay off a portion of your debt in exchange for a discount on your collateral.

- Execution: The smart contract instantly transfers your assets to the liquidator and uses the funds to pay down the protocol's debt.

One big risk here is the "liquidation fee." If a protocol charges too much-say 30% of the seized assets-liquidators might decide it's not worth the effort. This leads to "bad debt," where the protocol holds loans that are under-collateralized because no one wants to trigger the liquidation.

Traditional Government-Backed Liquidations

Contrast that with something like an SBA 7(a) Loan. This is a government-guaranteed loan for small businesses. If a borrower defaults here, the process is far more human and far more bureaucratic. The lender can't just click a button; they have to follow strict Standard Operating Procedures (SOPs).

In this scenario, the bank must prove they tried everything to recover the money before they can ask the government to pay out the guarantee. This involves site visits to inspect equipment, negotiating workout arrangements with the business owner, and conducting professional appraisals of the collateral. If those fail, they move to legal remedies like foreclosure or asset seizure. If the lender skips a step or fails to document the process correctly, the SBA might refuse to honor the guarantee, leaving the bank to eat the loss.

Complex Structures: Collateralized Loan Obligations (CLOs)

For institutional investors, there are Collateralized Loan Obligations (or CLOs). A CLO isn't just one loan; it's a giant pool of corporate loans bundled together. These are structured into "tranches" based on risk.

Liquidation in a CLO is more about managing a portfolio than chasing a single borrower. The lifecycle is divided into key phases:

- Reinvestment Period: For the first few years, managers can trade loans in the pool. If a loan looks like it's going to default, they sell it and buy a healthier one.

- Amortization Period: Eventually, the reinvestment stops, and the cash flowing in from the corporate loans is used to pay down the debt of the CLO itself.

Because CLOs are diversified across many different companies, they are generally more stable than a single DeFi loan. After the 2008 crisis, "CLO 2.0" structures added more credit enhancements to make sure the top-tier investors got paid even if some underlying loans went bust.

| Feature | DeFi Protocols | SBA 7(a) Loans | CLOs |

|---|---|---|---|

| Speed of Execution | Near-instant (seconds) | Slow (months/years) | Medium (managed portfolio) |

| Trigger Mechanism | Price Oracles/Code | Payment Default/Legal | Credit Rating/Cash Flow |

| Intermediary | None (Smart Contract) | Bank & Government | Collateral Manager |

| Primary Risk | Flash crashes/Bad debt | Regulatory non-compliance | Corporate defaults |

Common Pitfalls and How to Avoid Them

Whether you're a crypto trader or a business owner, the risks of liquidation are real. In DeFi, the biggest trap is "leveraged trading." If you use your loan to buy more collateral, you're amplifying your risk. A small price drop can trigger a cascade where you are liquidated, and the subsequent sale of your assets pushes the price down further, triggering other liquidations.

To protect yourself, consider these rules of thumb:

- Over-collateralize: Don't stick to the minimum ratio. If the limit is 110%, aim for 150% to give yourself a buffer against volatility.

- Set Alerts: Use monitoring tools to notify you the moment your collateral value drops, so you can add more assets before the smart contract takes over.

- Read the SOPs: For traditional loans, understand exactly what constitutes a "default." Sometimes a missed reporting deadline can be as damaging as a missed payment.

In the technical realm, DeFi protocols are starting to implement "grace periods." This is a window of time after a protocol is unpaused or a crash occurs, giving users a chance to top up their collateral before the automated liquidators pounce. It's a move toward a more "human" way of handling automated finance.

What happens to the remaining funds after a DeFi liquidation?

After the liquidator pays off the debt and takes their discounted portion of the collateral, any remaining funds generally go back to the borrower. However, the liquidator usually takes a specific percentage as a fee for performing the service.

Can I stop an SBA loan liquidation once it starts?

Yes, it is possible through a "workout arrangement." Because traditional loans involve human lenders, you can often negotiate a new payment plan or offer additional collateral to prevent the bank from seizing your assets.

Why do some DeFi loans get liquidated even if the price didn't change?

This usually happens because of accrued interest. Interest is added to your loan balance over time. If you don't pay it, your total debt grows while your collateral stays the same, which slowly lowers your collateral ratio until you hit the trigger point.

What is a CLO's "non-call period"?

The non-call period is a timeframe (usually 6 months to 2 years) during which the equity holders cannot "call" or refinance the debt tranches of the CLO. It ensures that the debt investors get a predictable return for a set period.

What is the role of the National Guaranty Purchase Center in loan liquidation?

The NGPC manages the final stage of SBA loan liquidations. Once a lender has exhausted all collection efforts and liquidated the collateral, they apply to the NGPC to purchase the guaranteed portion of the loan, essentially getting reimbursed by the government for the loss.

Next Steps for Borrowers

If you are currently managing a collateralized loan, your priority should be a risk audit. For crypto users, check your health factor on your dashboard daily. If you are in a traditional business loan, ensure your financial reporting is up to date and your collateral assets are properly insured.

For those looking to enter the market, the lesson is clear: liquidity is a double-edged sword. It gives you immediate capital, but it ties your future to the market price of your assets. Always assume the market will move against you and build your collateral buffers accordingly.

Sean Mitchell

April 17, 2026 AT 15:45Absolutely catastrophic that we're just accepting this digital guillotine as a normal part of finance. The sheer horror of losing a portfolio to a mindless script is simply too much to bear!

nikki krinkin

April 18, 2026 AT 21:45It's pretty wild how different these systems are. I can see why people get nervous about the speed of DeFi.

Adedamola Oyebo

April 19, 2026 AT 19:14Price oracles are a single point of failure!!! Always check if a protocol uses Chainlink or a custom oracle... it matters!

Mark Pfeifer

April 20, 2026 AT 16:24I'm curious if the grace periods in DeFi will eventually lead to more systemic risk by slowing down the liquidation process during a crash.

Michelle Stanish

April 21, 2026 AT 05:30Too much risk.

Abhinav Chaubey

April 21, 2026 AT 19:16Obviously, anyone with a brain knows that the Indian market handles volatility much better than these fragile US-centric models. I've seen better risk management in a local kirana store than in some of these DeFi protocols.

Michael Harms

April 23, 2026 AT 16:34Great breakdown of the concepts! Keep pushing through the learning curve, everyone. We can all master this with a bit of patience and a solid strategy!

Kim Smith

April 23, 2026 AT 21:30it is kinda funny how we think we are evolveing by moving from paper to code but we're really just changing the flavor of the anxiety we feel... like, in the old days you'd wait for the man in the suit to take your keys and now you just refresh a webpage and see a red number... its all just a cycle of trust and betrayal in the grand scheme of human exchange and maybe we are just meant to lose things to the void anyway lol

Keri Pommerenk

April 25, 2026 AT 19:53just keep your health factor high and you'll be fine let the bots do their thing while you sleep soundly

Joshua Salwen

April 26, 2026 AT 14:26I can't believe I have to explain this but the

Joshua Salwen

April 27, 2026 AT 16:28...the discrepancy between CLO 2.0 and original structures is where the real carnage happened, and most people just ignore the tranche haircutting process entirely! It's an absolute joke!

Luke George

April 27, 2026 AT 18:21The oracles are probably controlled by the same people running the banks anyway. It's all a closed loop to make sure the house always wins while we think we're using

Anna Grealis

April 29, 2026 AT 05:03Probably just a way to steal money from retail investors with fancy words like

Anna Grealis

April 30, 2026 AT 11:04...amortization. Typo in the article probably just means they want to confuse us more.

Yuhan Mo

May 2, 2026 AT 10:50The delta between the liquidation threshold and the actual market price is where the real alpha lies for the liquidators. It's essentially a race to the bottom in terms of latency.

Karen Mogollon Gutierrez

May 2, 2026 AT 15:40It is truly an affront to the dignity of the borrower that one must submit to the whims of a computer program without the courtesy of a formal notice. One finds the lack of professional decorum in the DeFi space to be utterly abhorrent!

Shannon Kelly Smith

May 3, 2026 AT 12:08Just remember to stay diversified! 🚀 Use a mix of stables and volatile assets to keep that ratio healthy! You got this! 💪

John and Lauren Busch

May 4, 2026 AT 22:17Sarcasm intended, but sure, let's just trust the

John and Lauren Busch

May 5, 2026 AT 06:08...code to handle our life savings. Seems totally safe.

Jeff Barlett

May 6, 2026 AT 07:26Wait, why are we pretending traditional loans aren't just as predatory? They just use more stamps and ink to make you feel a false sense of security. It's a total circus!

Kaitlyn Wu

May 6, 2026 AT 08:08If you're borrowing against assets, you need to be the most disciplined person in the room. No excuses. Set your alerts and don't let your ego override your risk management.

Thomas Jewett

May 7, 2026 AT 10:08The American way of business is under attack by these digital scams and we need to return to real assets like land and steel not some fake numbers on a screen that can disappear in a second becuse of a glich in the code which is just a cover for the people stealing our money!!!

nathan jones

May 7, 2026 AT 12:38Pretty straightforward explanation of the basics.

Tracy Sperandio

May 8, 2026 AT 00:56Listen up, you absolute legends! If you want to thrive in this financial jungle, you've got to be proactive! Stop playing it safe and start dominating your portfolio with a vivid strategy that leaves the liquidators in the dust! Let's get those gains and keep those ratios sparkling!