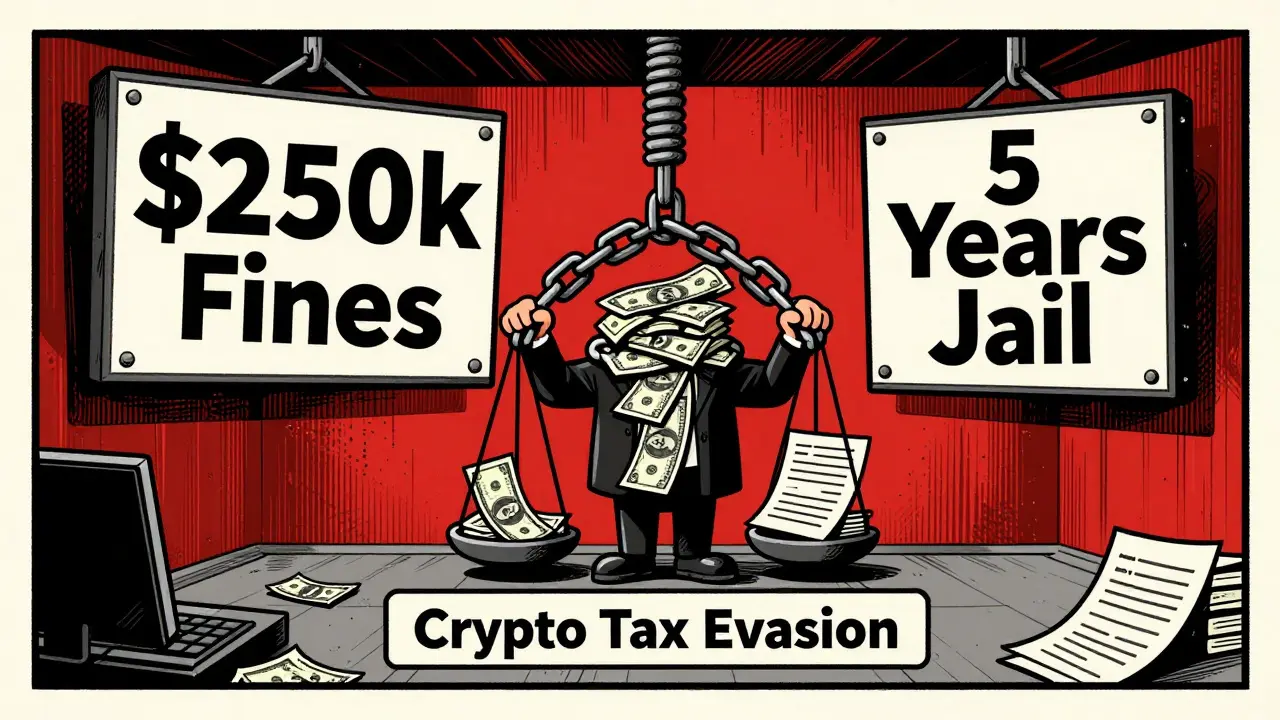

You might have thought that moving your Bitcoin to a private wallet or trading on a decentralized exchange kept you off the radar. That era is over. The Internal Revenue Service (IRS) now treats cryptocurrency tax evasion as a serious felony, carrying maximum criminal penalties of up to 5 years in prison and fines reaching $250,000. This isn't just about forgetting to report a small gain; it's about intentional non-reporting in an environment where blockchain analytics make every transaction visible.

If you hold digital assets, the rules changed dramatically starting January 1, 2025. With the introduction of new reporting standards and enhanced tracking capabilities, the window for 'voluntary' correction is closing fast. Here is what you need to know to avoid becoming a statistic in the next wave of enforcement actions.

The New Reality: Crypto Is Property, Not Cash

To understand why the penalties are so severe, you first need to understand how the law views your holdings. The IRS classifies cryptocurrency as property rather than currency. This distinction is critical. It means that every time you trade, sell, mine, stake, or even receive crypto as payment, you trigger a taxable event. You don't get the same anonymity you would with physical cash under a mattress. Every transaction leaves a permanent, immutable record on the blockchain.

This classification creates a comprehensive enforcement framework. Intentional failure to report this income constitutes criminal tax evasion, which is distinct from civil tax avoidance. While avoiding taxes through legal strategies like tax-loss harvesting is permitted, hiding income is not. The IRS has made it clear that there is no minimum threshold for reporting. If you earned $10 worth of crypto activity, it must be disclosed on your tax return. Ignoring these obligations because they seem small is a dangerous gamble.

Operation Hidden Treasure: How They Find You

The biggest myth in the crypto community is that decentralization equals anonymity. The IRS has dismantled this idea through programs like Operation Hidden Treasure utilizes advanced blockchain analytics. These tools allow the agency to trace unreported transactions across major networks, linking wallet addresses to real-world identities through exchanges, KYC (Know Your Customer) data, and IP address logs.

Consider the case of a user who moved funds from a centralized exchange to a self-custody wallet to hide gains. In the past, this might have worked. Today, forensic firms used by the IRS can analyze years of historical blockchain data. They can identify patterns, cluster addresses, and pinpoint exactly when and where taxable events occurred. Retroactive enforcement is common. Just because you didn't report gains in 2021 doesn't mean you're safe in 2026. The IRS can look back several years, applying penalties and interest to unpaid obligations.

The Cost of Non-Compliance: Fines and Prison

Let’s talk numbers. The headline penalty is $250,000 in criminal fines and five years in prison. But the financial damage often goes deeper. Civil penalties for crypto tax violations can actually exceed the criminal fines. Here is how the math works against you:

- Base Criminal Fine: Up to $250,000.

- Federal Prison: Up to 5 years.

- Failure-to-Pay Penalty: Up to 25% of unpaid taxes.

- Failure-to-File Penalty: Up to 25% of unpaid taxes.

- Interest Charges: Accumulate daily on all unpaid amounts.

In total, you could face combined penalty rates of 75% of your original tax obligation, plus the criminal fine. For someone who owed $50,000 in taxes, the penalties alone could push the bill over $100,000, not counting the risk of incarceration. This severity applies equally to crypto violations as it does to traditional tax evasion, but detection is far easier due to the transparent nature of ledger technology.

| Penalty Type | Traditional Tax Evasion | Crypto Tax Evasion |

|---|---|---|

| Maximum Imprisonment | 5 Years | 5 Years |

| Maximum Criminal Fine | $250,000 | $250,000 |

| Detection Difficulty | High (Cash-based) | Low (Blockchain-traceable) |

| Civil Penalties | Up to 75% | Up to 75% |

| Retroactive Enforcement | Limited | Extensive (Historical Data) |

2026 Rules: What Changed for Investors

If you are filing taxes for the 2024 tax year (due April 2025) or preparing for 2025 filings in 2026, you need to know about two major regulatory shifts that took effect on January 1, 2025.

First, the Form 1099-DA requires U.S. cryptocurrency exchanges to file detailed reports for digital asset transactions. Previously, many platforms did not report your trades to the IRS unless you withdrew fiat currency. Now, exchanges must provide comprehensive transaction data. This gives the IRS a direct line to your trading history, making it nearly impossible to claim you 'forgot' about a sale if the government has a record of it.

Second, the accounting method changed. Investors can no longer use a universal accounting method for cost basis calculations. Instead, you must use wallet-by-wallet accounting involves tracking transfers between different wallets and exchanges separately. This means you need detailed records of every transfer, including self-transfers between your own personal wallets. If you move Bitcoin from Wallet A to Wallet B, that is a recordable event that affects your cost basis. Failure to track these moves accurately can lead to unintentional underreporting of gains, which the IRS may interpret as negligence or worse.

Avoidance vs. Evasion: Know the Difference

Not all tax planning is illegal. There is a clear line between legal tax avoidance and criminal tax evasion. Understanding this difference can save you from federal charges.

Tax Avoidance (Legal): Using legitimate strategies to minimize liability. Examples include holding crypto for more than one year to qualify for long-term capital gains rates, using tax-loss harvesting to offset gains, or investing through retirement accounts like IRAs where applicable.

Tax Evasion (Illegal): Intentionally concealing income or misrepresenting facts. This includes failing to report staking rewards, ignoring mining income, deleting transaction histories, or using mixers/tumblers specifically to obscure the trail of taxable events. Even if the amount is small, the intent matters. If you knowingly omit information, you are committing a felony.

How to Comply in 2026

So, how do you protect yourself? The best defense is proactive compliance. Here are the steps you should take immediately:

- Gather Records: Export transaction histories from all exchanges, wallets, and DeFi protocols. Include dates, amounts, transaction types, and counterparties.

- Use Specialized Software: Platforms like Koinly, CoinLedger, and CryptoWorth automate tax reporting and cost basis calculations. These tools connect to your wallets and exchanges to generate accurate reports, reducing the risk of human error.

- Calculate Cost Basis Correctly: Ensure you are using the wallet-by-wallet method required since 2025. Verify that self-transfers are accounted for properly.

- File Amended Returns: If you missed reporting crypto income in previous years, file amended returns voluntarily. The IRS often offers reduced penalties for voluntary disclosure compared to enforcement discoveries.

- Consult a Professional: Crypto tax law is complex. A CPA specializing in digital assets can help navigate the nuances of staking, airdrops, and DeFi interactions.

Community feedback from forums like r/CryptoCurrency shows widespread anxiety about retroactive penalties. Many users report receiving IRS letters questioning unreported income. Those who acted quickly by filing amended returns generally faced lower penalties than those who waited for an audit. Do not wait for a letter in the mail. Take control of your situation now.

Global Context and Future Outlook

The U.S. is not acting alone. Global crypto compliance penalties reached $5.1 billion in 2024, a 39% increase from the previous year. The United States accounted for $2.4 billion of that total. While much of this was related to anti-money laundering (AML) and KYC violations, tax evasion triggered 15% of enforcement actions globally. The trend is clear: governments are dedicating significant resources to closing loopholes.

Looking ahead, industry analysts predict that while political rhetoric may shift, enforcement of existing tax obligations will remain strict. The combination of blockchain analytics, mandatory exchange reporting via Form 1099-DA, and severe criminal penalties creates a framework designed for total transparency. The days of operating in the shadows are over. Compliance is no longer optional; it is the only way to secure your financial future without risking freedom or fortune.

What happens if I don't report my crypto taxes?

If you intentionally fail to report crypto income, you face criminal tax evasion charges. Penalties include up to 5 years in prison, $250,000 in criminal fines, and civil penalties up to 75% of unpaid taxes. Interest also accumulates on all unpaid amounts.

Does the IRS track private wallets?

Yes. Through programs like Operation Hidden Treasure, the IRS uses blockchain analytics to trace transactions on public ledgers. If you ever interacted with a KYC-compliant exchange, they can link your identity to your private wallet addresses.

What is Form 1099-DA?

Form 1099-DA is a new IRS form that requires U.S. cryptocurrency exchanges to report detailed digital asset transactions. Starting in 2025, this provides the IRS with comprehensive data on your trades, making unreported income much easier to detect.

Can I fix past mistakes by filing amended returns?

Yes. Voluntary compliance by filing amended returns for previous years often results in reduced penalties compared to being caught in an audit. It demonstrates good faith and can prevent criminal prosecution.

Is tax avoidance legal?

Yes, tax avoidance is legal. It involves using legitimate strategies like long-term holding for lower capital gains rates or tax-loss harvesting. Tax evasion, which involves hiding income or lying on returns, is illegal and carries severe penalties.